By Lucy Komisar

June 6, 2021

The Securities and Exchange Commission, set up after the 1929 stock market crash, has been a corrupt operation captured by the stock brokers and Wall Street actors it was supposed to regulate. Here is the history, told in text and in a video I did for Superstonk.

Here is a slideshow that tells the story.

How the SEC was created

One reason for the stock market collapse in 1929 was watering the stock. A meme went “He who sells what isn’t his’n must pay it back or go to prison.” Traders would print up counterfeit stock certificates. Sound familiar. Naked short selling. Provoked the crash that started the depression.

1932 Ferdinand Pecora was an immigrant working class kid from Sicily who put himself through New York Law School. He was hired in 1932 by the Senate Banking Committee to investigate the causes of the crash, to do a whitewash, but he didn’t get the memo. His hearings exposed such practices as pools to support bank stock prices. Such as Let’s all coordinate trades to pump up the stock. Sound familiar? GameStop? National City Bank (now Citibank) had hidden bad loans by packaging them into securities and selling them off to unwary investors. Sound familiar? Mortgage-backed securities that tanked? And that the bank sellers knew would tank?

The findings of the Pecora Commission exposing corruption of the financial industry let to public support for regulation, — it took really dirty stuff to move the pubic -which would be the Glass–Steagall Banking Act of 1933, the Securities Act of 1933, and the Securities Exchange Act of 1934. That last set up the SEC.

Franklin Roosevelt appointed Joseph Kennedy (father of Jack and Robert) SEC chair. He had built the family fortune on financial manipulation, but Roosevelt thought he knew where the bodies were buried, who the miscreants were. So the SEC cleaned up the Wall Street stables for five years. Then Kennedy’s buddies of the financial oligarchy took charge again, in early regulatory capture.

Pecora wrote a memoir, “Wall Street Under Oath.” He said: “Bitterly hostile was Wall Street to the enactment of the regulatory legislation.” What, the thieves don’t want rule of law? About disclosure rules, he said that, “Had there been full disclosure of what was being done in furtherance of these schemes, they could not long have survived the fierce light of publicity and criticism. Legal chicanery and pitch darkness were the banker’s stoutest allies.” Think about who their allies are today.

1985 Irving Pollack

Fast forward about half a century. With the support of friends in Congress, Wall Street has neutered the securities acts by assuring the SEC would not enforce them. It made sure its foxes were guarding the henhouse. But the corruption was sometimes inconvenient. In 1985, the National Association of Securities Dealers, now FINRA, which represents the brokers, hired Irving Pollack, a former SEC commissioner who was honest, to look at short selling.

Among his report’s proposals: reporting of short interest – the amount of short sales not yet covered — should be public and perhaps more frequent. A borrowing for delivery in broker-dealer transactions should be required. A mandatory buy-in should be adopted for a delivery after a reasonable period when there has been a fail. That means the broker for the buyer who hasn’t gotten the shares can buy them on the market and charge the short seller’s broker. There should be surveillance of large short-interest positions, shorts not yet covered.

Did the SEC adopt these proposals with enthusiasm? Obviously not. Short interest is not reported frequently. Broker dealers “locate” instead of borrow or they use counterfeit shares. There’s no buy-in. Buy-ins were allowed but not required. And Leslie Boni, an academic who in 2004 did a paper for the SEC on buy-ins said they were rare. But requiring buy-ins would make the stock go up, the shorts lose money.

And there was no surveillance of large short-interest positions.

In fact, corruption would be increased thanks to friends of Wall Street president Bill Clinton and his collaborator Treasury Secretary Robert Rubin (formerly of Citibank) who in 1999, killed the Glass-Steagall Act which had separated investment banking from retail banking. Retail banks till then could not use depositors’ funds for risky investments. Only 10% of their income could come from selling securities.

That sets the stage for the last few decades.

2004 RegSHO set up to fail

The SEC, battered with complaints, in July 2004 promulgated Reg SHO, SHO for short selling. The hedge funds and big brokers who had been or would be shown to be illegally shorting all lobbied against it. It was a tepid reform of short selling that was Swiss-cheesed with loopholes. Think of Al Capone writing the tax laws. (On the other hand, his crooked progeny do write the tax laws!) Reg SHO would be implemented in 2005.

The SEC knocked out a proposal for penalties for failing to deliver. And it wrote two giant exceptions into Reg SHO. Ex-clearing and market makers.

The rule didn’t apply to ex-clearing, which means clearing outside the DTCC, the Depository Trust Clearing Corporation, the national stock clearing company. (Yes, it’s a private company owned by the broker dealers.) It applied only to trades going through a registered clearing agency, i.e. what got sent through the DTCC. It said ex-clearing was “rare.”

Sales that avoided clearing agencies could fail – not be delivered — without buyers’ brokers reporting the fails to the DTCC or buying in, requiring the short sellers broker to buy shares on the market and deliver them. To protect short sellers and avoid Reg SHO, dealers went ex-clearing. They either cleared internally or with a cooperating broker-dealer or they went through dark pools. They were private exchanges set up by the big prime brokers and banks.

The major perpetrators of naked short selling are the large banks/prime brokers, doing it for large clients, hedge funds, or their own accounts. If they can do the transaction privately [ex-clearing], RegSHO doesn’t apply. Now about 40% of trades go through dark pools. If a trade failed ex-clearing, it didn’t fail at the DTCC!

Reg SHO also didn’t apply to derivatives, the financial casino bets acknowledged as a prime cause of the current economic crisis and which also did not trade through a clearing house.

Even stocks that cleared through the DTCC were not always covered. The brokers got a “grandfather clause” that allowed existing fails to continue! Because we know that brokers simply rolled them over. And brokers didn’t have to close out the shares they had sold short before the stock went on the Threshold List which includes shares that for five consecutive settlement days had fails to deliver of 10,000 shares or more at a clearing agency and where the level of fails was equal to at least one-half of one percent of the issuer’s outstanding shares.

Then brokers were subject to mandatory covering only on the fifth day. Then the broker-dealer had 13 days to deliver the shares to the buyer or lender, and if it failed to do so, it could not trade that stock until it did. But the SEC knew, because staff wrote a paper on it, how options conversions allowed brokers to put off fail dates forever.

MARKET MAKERS

Reg SHO allowed an options market maker exception, called after the person who designed and pushed for it: the Madoff Exception! (Did I say the crooks wrote the rules?)

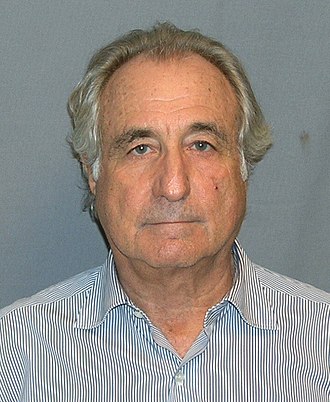

Bernie Madoff, who died in prison in April 2021, in 2012 told Forbes journalist Diana Henriques: “I fell into my crime of staying Naked Short. The fact that the prosecutor and Trustee seemed clueless of this is why my frustration is so great.” Clueless, or complicit? You just don’t go there.

The SEC in 2007 eliminated Uptick Rule that requires short sales to be conducted at a higher price than the previous trade. Not helpful if the purpose is to batter down the stock price. It was never enforced.

2008 Stock lending and taking care of the banks

According to the SEC Office of Economic Analysis (2008) Reg SHO in effect since 2005 had not reduced outstanding fails. Many stocks remained on the SEC Regulation SHO Threshold List for hundreds of trading days

For years, the SEC claimed naked short selling and fails to deliver were not a problem. Once things began to go sour in 2008, the first thing the SEC did was ban naked short selling in 17 financial stocks plus Fannie and Freddie. It was ironic, since the big banks/brokers had been carrying out the scam on others. Hoist on their own petard.

And they chose the solution that people battling naked short selling had advocated for years. A July 2008 order said no traders could make trades involving those institutions unless they had pre-borrowed the security or otherwise had it available in their inventory. They had to deliver the security on the settlement date. All the regs that came out were because naked shorting, the counterfeiting of shares, was undermining banks. The SEC went from nothing is happening till the fall of 2008 that the market is coming apart because of naked shorting. They chose the solution that people battling naked short selling had advocated for years. Borrow shares before you sell them short. Stop the counterfeiting.

The SEC said it was investigating the collapse of Bear Stearns. It had been massively naked shorted. The commission didn’t come up with anything it made public.

2009 Kaufman and the hard locate

A little-known backstory involved then Delaware Senator Ted Kaufman who most recently ran Biden’s post-election transition team. It shows how big stock market players and the institutions they control have blocked attempts to deal with naked short selling. Kaufman was Biden’s longtime chief of staff and was named to the Senate seat vacated by his boss when Biden became Barack Obama’s vice president.

After the 2008 market meltdown that included abusive naked short selling of Bear Stearns and Lehman Brothers, Kaufman, a Democrat, and Georgia senator Johnny Isakson, a Republican, introduced legislation that directed the SEC to write regulations to end the practice. They determined that the SEC’s current regulations were unenforceable. Hedge funds could spread rumors, do massive shorts without locating stocks, and deliver after the prices dropped.

In July 2009, Kaufman and six colleagues from both parties wrote to the SEC proposing a “hard locate” plan that would ban all short sales unless the executing broker first obtained a unique identification number for the shares, perhaps through an automated centralized system. This would prevent multiple short sales on the basis of a single share.

According to Jeff Connaughton, then Kaufman’s chief of staff, months before the letter, “the DTCC (the national stock clearing agency) had gone to the SEC with a proposed solution to naked short selling that looked like Kaufman’s solution, with the DTCC creating a centralized database that would prevent the same shares from being used for multiple short sales.

The DTCC told Connaughton, ‘We got pulled back.’ They meant, he said, by their board, by the Wall Street powers-that-be.” Because in the case of the DTCC as well as the SEC, the fox is guarding the henhouse. Connaughton wrote about this in his book, “The Payoff: Why Wall Street Always Wins.”

In 2009 staffers of the senators met with the SEC’s Enforcement Division to find out the status of its investigation into the naked short selling of Bear Stearns and Lehman stock. SEC lawyers told them they’d have to be patient and that the investigation would take at least another year. It never happened. Or at least the results were not made public.

There were some alleged improvements made that year, 2008.

The market makers exemption was eliminated, because the SEC said substantial levels of fails had continued in Threshold Securities, and a significant number were the result of market maker exceptions. But they still had 6 days to settle their trades. So you have market makers failing and rolling their shares over every 5 ½ days.

The grandfather provision on Threshold Securities was eliminated. Unless its position in Threshold Securities was closed, a broker-dealer couldn’t effect further shorts in them without borrowing or arranging to borrow the securities. They finessed that.

The amendments addressed fake borrows. It said that where a broker-dealer entered into an arrangement with another party to purchase or borrow securities, and the broker-dealer knew or has reason to know that the other party would not deliver securities in settlement of the transaction, the purchase or borrow would not be “bona fide.”

It repeated that: “The NSCC – clears and settles the majority of equity securities trades conducted on the exchanges and in the over-the-counter market.”

So the rules still didn’t apply to ex-clearing and dark pools. The ex-clearing route to naked shorts was protected. Fails could be concealed at the start by ex-clearing, by not reporting them to the NSCC, the National Securities Clearing Corporation.

In fact, the dealers could use ex-clearing to opt out of fails from trades through the exchanges. They could take them onto their own books and deal with the fails as they chose to, meaning do nothing, let the fails sit.

And protecting the interests of the big banks/brokerages, the SEC did not include a hard locate requirement in its amendments to Reg SHO.

2010 Kaufman continued to try to fight naked short selling in the Dodd-Frank debate. SEC had been ordered by the Dodd-Frank law of 2010 eleven years ago to require more transparency in short selling and stock lending. It has ignored it.

The SEC occasionally takes enforcement actions that go after low-hanging fruit, ie don’t bother anyone significant or don’t order more than minor penalties, the cost of doing business. Take a look back.

2003 Sedona/Badians

The Sedona case, where the Badian brothers of Vienna, Austria, ran a death spiral financing scheme that in 2001 involved providing a loan that would be repaid in shares. And then it did a massive shorting attack that knocked down the price of the shares from $6 to 20 cents. The SEC in February 2003 filed a complaint against Thomas Badian and his company, Rhino, for fraud and market manipulation of Sedona shares. Badian and Rhino immediately settled with the SEC for a $1-million fine without admitting or denying guilt. The $1 million was a pittance, cost of a crook doing business.

In 2006, the SEC filed a civil suit against Andreas Badian, four officials of Pond Equities and a trader at Refco, all involved directly in the naked shorting, but not against Ladenburg Thalmann, the high-profile broker-dealer that facilitated the deals and collaborators.

2005 Eagletech

Eagletech, which had an invention, new at the time, to push phone calls to other devices, letting people use a single phone number that followed them from phone to phone. He became a target of a group of death spiral financing criminals working with Salomon Smith Barney in New York, five Salomon officers and a group of investors offering to buy convertible preferred shares from Eagletech for up to $6 million.

They did a pump up and then naked shorting so the stock dropped from $14 to 75 cents, reducing the market value by $113 million. The stock went to 2 cents. The FBI was investigating organized crime stock market fraud. They busted 17 members of the mob, including the malefactors who ran the scheme against Eagletech.

SEC filed suit against mob leaders Serubo, Labella and their organized crime collaborators who got control of Eagletech stock. It said they generated over $12.7 million from the scam. Members of the Salomon Smith Barney financing team and their options market-makers in Chicago were selling shares and then failing to deliver.

Serubo, Labella and their henchmen would be banned from penny stock trading, fined and ordered to pay back their ill-gotten gains. No penalties against the Salomon Smith Barney team or their options market maker collaborators.

Then the SEC filed suit against the victim, Eagletech, to deregister its shares, because it couldn’t afford several hundred thousand dollars to file audited financial reports. The delisting is like a bankruptcy, all investors are wiped out and the naked shorters never have to cover. The SEC finished what the mob started, it killed the company.

2007 Goldman

From at least March 2000 to May 2002, more than two years, certain customers of Goldman Clearing used the firm’s direct market access, automated trading system to unlawfully sell securities short in advance of follow-on and secondary offerings when they could get the shares cheaper.

They were selling the offered securities short, using Goldman Clearing’s REDI System, preparing their own orders to sell on computer terminals and falsely marked them “long.” The orders were routed directly to the New York Stock Exchange and other markets for execution.

Goldman Clearing’s own records contained information that customers were selling short and that they were misrepresenting their “short” sales as “long.” Goldman Clearing’s records showed that the customers were repeatedly failing to deliver to Goldman Clearing the securities that they purported to sell long.

So, for two years of allowing shorts to be marked longs, Goldman had to pay civil money penalty of – wait for it — $1 million

2012 SEC v OptionsXpress

OptionsXpress, a wholly-owned subsidiary of Charles Schwab, repeatedly engaged in sham transactions, known as “resets,” designed to give the appearance of having purchased shares to close-out an open fail-to-deliver position while in fact not doing so.

OptionsXpress had its customers buying shares and simultaneously selling call options that were the equivalent of selling shares short. The purchase of shares created the illusion that the firm had covered the short; however, the shares were never actually delivered to the buyers because on the same day, calls were exercised, effectively reselling the shares. The purpose was to perpetuate an open short position.

In 2009, the six optionsXpress customer accounts bought $5.7 billion worth of securities and sold short approximately $4 billion of options. They did this to a couple of dozen companies. In January 2010, the customers who did the scam accounted for 48% of the daily trading volume in Sears. In the end OptionsXpress had to pay $4 million. Cost of doing business.

The insiders tell the SEC corruption

The story of Gary Aguirre says it all

As a student at Georgetown Law School, Aguirre got a prize from the SEC for a paper on Wall Street corruption as detailed in the Pecora hearings that led to passage of the Securities Act of 1933. So we know where he stands. In September 2004, he started as a senior counsel at the SEC Division of Enforcement. He said, “I understood what SEC was supposed to be doing: keep Wall Street from running amok.” The SEC in July had promulgated Reg SHO, which it said would stop abusive naked short selling. He recalled, “The first thing I noticed is there seemed to be a deference to the large law firms who represented Wall Street players. And there were a lot of people there not at the same skill set level as the attorneys representing some of the players from Wall Street.”

Aguirre was assigned to an investigation that implicated a powerful Wall Street insider. John Mack had been head of the hedge fund Pequot Capital Management. The suspicion was that Mack had tipped Pequot’s then CEO, Arthur Samberg, of General Electric’s pending acquisition of Heller Financial. Mack was the only suspect. Without that investigation, the SEC would never be able to even consider the filing of insider trading charges against Mack, Samberg, Pequot or anyone else arising out of Pequot’s trading in GE and Heller.

An SEC official told him it would be very difficult to take Mack’s testimony, because of his political influence. He told him that Mack was “an industry captain,” that he had powerful contacts . . . , that Mary Jo White could contact a number of powerful individuals, any of whom could call Linda about the examination. Mary Jo White was a lawyer at a Wall Street firm, Linda was Linda Thomsen, the head of enforcement. Aguirre confirmed the conversation in two e-mails to the official the next morning. The first email referenced Ferdinand Pecora.

Aguirre refused to stop his investigation. Senior officials in the SEC’s Division of Enforcement blocked an SEC subpoena seeking Mack’s testimony and records in the investigation. Aguirre had contacted the Office of Special Counsel to discuss the filing of a complaint about the SEC’s protection of Mack. Three days later, on September 1, 2005, while on vacation, Aguirre was abruptly fired by phone.

Aguirre gave key papers to Charles Grassley on the Senate Finance Committee. And to the Judiciary Committee. There were hearings in 2006.

He told Congress what the SEC official had told him about political influence, about how Mary Jo White could contact powerful individuals who could call Linda Thomsen.

Aguirre said the SEC “favor” to Mack cleared the way for his return on June 30, 2005, as Morgan Stanley’s CEO with no danger of an SEC lawsuit for insider trading. Mary Jo White would become chair of the SEC 2013 to 2017, appointed by Wall Street’s favorite guy, Barak Obama, who apparently didn’t know the Aguirre story. More likely he did and didn’t care.

Later David Kotz, the SEC’s inspector general, said he had found evidence that “raised serious questions about the impartiality and fairness” of the SEC’s investigation of possible insider trading at the Pequot Capital Management hedge fund.

Kotz also condemned what he called the “common practice” of giving outside lawyers’ clients access to high-level SEC officials when they had complaints about front-line investigators. Kotz made numerous recommendations for reform, which the SEC ignored.

Aguirre sued the SEC and won $772,000 in back pay and damages.

Mack, after being CEO Morgan Stanley, became CEO of Credit Suisse, then chair of Morgan Stanley and now is senior advisor to the global investment firm Kohlberg Kravis Roberts, whose strategic partners are hedge funds.

2005 Fickes and Overstock and Chris Cox

Here’s another case of an SEC staffer who tried to do the right thing but was pulled back. In August 2005, Overstock.com filed suit against hedge fund Rocker Partners and the equities research firm, Gradient Analytics. It said the hedge fund was short-selling the company while paying for negative Gradient reports to drive down share prices.

Overstock CEO Patrick Byrne took his information to Mark Fickes of the SEC San Francisco office. He said, “Look at the patterns, their stocks are naked shorted by Dan Loeb, David Einhorn, Steven Cohen, David Rocker. [Look at] the dates journalists Bethany, Boyd, Remond, Greenberg wrote trash jobs. [That was Bethany McLean writing for Fortune, Carol Remond for Dow Jones, Roddy Boyd for the NY Post, Herb Greenberg for MarketWatch.] Byrne said, “It was the same pattern, each one of these journalists writes a hatchet job, there is naked shorting, SEC action begins against them, and the Milberg Weiss lawsuit. In every case, it’s part of same bum rush on the stock.”

Byrne argued that Gradient, an investment advisor putting out fraudulent reports the shorters used, should be investigated – and that the journalists were central to his case. Subpoenas were issued to Carol Remond and Herb Greenberg to provide information about conversations that they had with stock traders and analysts.

Fickes issued the subpoenas with the approval of the SEC’s head of enforcement, Linda Thomsen. It was announced that the SEC was investigating Gradient and had issued subpoenas to Carol Remond, Herb Greenberg and to Jim Cramer of TheStreet. David Rocker sold his shares in TheStreet. A month later Cramer sold some of his shares.

Bryne: “Jim Cramer gets a subpoena; you have three days to disclose it. He knows TheStreet will crater, he can’t just go sell it with undisclosed material information. He can get a plan to sell x amount per quarter after he gets the subpoena. TheStreet broke under a dollar.”

“Why would a hedge fund guy have an interest to own a financial publication? Cramer discloses in his books stuff that is widely illegal. Protection for journalists is about protecting sources about stories they are writing, not about their own corrupt market manipulation.”

The question is whether freedom of the press extends to reporters whose articles are part of illegal naked short selling scams. Fickes wanted to know.

He was summoned to Washington to meet with the new SEC chair, Cris Cox. Ultimately, Byrne said, the SEC caved under the media pressure. Cox killed the subpoenas and the SEC dropped its investigation of Gradient. Cox was SEC chair when Gary Aguirre was fired.

What should the SEC do now? Solutions are there if it wants to protect investors, not do as it is told by the big broker-dealers.

- Require buy-ins. Require the broker of the investor who doesn’t get shorted stock delivered to buy it on the market and charge the seller’s broker. Of course, requiring buy-ins would make the stock go up, the shorters lose money.

- Restore the uptick rule so shorters can’t sell for less that the last shorted trade. That would stop shorters hammering a stock down to bankruptcy.

- Create a consolidated audit trail (CAT) to collect order and trade execution information to identify and enable punishment of illegal trading activities, including naked short selling. More than a decade after the SEC promised it, following the 2010 flash crash, CAT doesn’t exist.

- Impose real penalties on transgressors, like loss of license.

- Send cases of serial trading cheats to the Justice Department for criminal prosecution.

- End the revolving door with Wall Street.

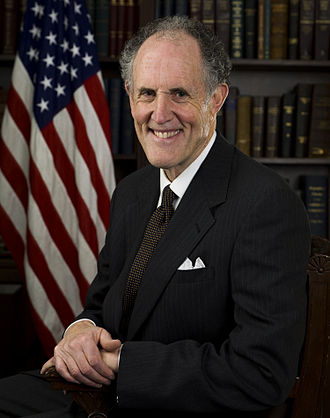

- What will Gary Gensler do? And will he listen most to the pushback from the big brokers or investors like people on Superstonk?

I tagged you on Twitter also with this statement. Gary Gensler is NOT our friend. He’s already talking about rules to protect individual (stupid money) investors to protect them from their “stupid” investments. What he doesn’t mention is any problem with naked short selling or why the SEC doesn’t enforce their own rules. He is part of the 1% and in bed with the criminals breaking the rules. I don’t think we will see any help or solutions come from him. It’s going to take an awakening of the American people to understand what’s going on and that’s going to be an uphill battle because mainstream media also belongs to the 1%. It’s going to take people like you and Wes Christian and Susanne Trimbath and God only knows what else to wake up people to the corruption.

don’t expect any help from Gary Gensler, he is already talking about how to protect “stupid money” from themselves. He doesn’t mention anything about naked shorts and what he might do about that. He is in bed with the corruption and will not stop it. It’s going to take people like you and Wes Christian and Susanne Trimbath and millions of Americans standing up against the corrupt practices of wall street. this is my second reply and don’t know why the first one doesn’t show up. Hope this one goes through

The justice dept ✌️

Great job as always Lucy; glad I found your site! Loving all of this info. Take care.

What about Jeffrey Harris et al. and his exposition of Nasdaq MM corruption and their use of 1/8th amounts to manipulate. Their piece led to a DOJ investigation and directly impacted the formation of FINRA and other regulations.

https://www.onlinelibrary.wiley.com/doi/abs/10.1111/j.1540-6261.1994.tb04783.x

Pingback: Mirror: The corruption of the SEC, over decades and till today, Lucy Komisar – Robert David Steele

Thanks you for all you do!!

Great work uncovering the corruption on wall street and regulatory capture of the SEC. This is blatant fraud at the highest levels. I dont have much faith in Gensler in enacting any regulations to curb short selling and media manipulation, I guess only time will tell

Thank you for your amazing investigative reporting and support of the retail investor. This corruption must come to an end.

Wow, Great reporting.

One problem I see here,

The fact that now you will

Be accused of being off your

Rockers!!

We know otherwise.

Great Work.

LK: “Ad hominem” means attacking a person’s character or motivations rather than a position or argument. That is what the defenders of the corrupt stock market system often do. Because they have no real arguments.

Whoever said that markets are fair and equitable with little to no price fixing was either stupid, incredibly naive or works for the SEC.

Thank you so much for everything you have done to shine light on the corruption and fraud that has poisoned our markets for far to long. Amazing article !

Loved this, Lucy!

Amazing article, Lucy! Thank you for everything you’ve done to the Superstonk community!

Thank you for all you do!

Good write up

Interesting article. Suggest doing a story (refer to SEC/DOJ for prosecution, also?) on current Boeing (BA) stock price manipulation (likely naked shorting by market maker/dark pools/big brokers?) – down the past few weeks even on good news days… Some of the usual suspects in the media (Jim Cramer (CNBC), etc.) appear involved again. A big plane sale to United was mentioned coming next day, but Cramer was quoted as saying the stock wouldn’t go up much the next day (it went down 4 points for the day), which defied logic when largest plane sale in decade for Boeing. A 40 year old plane crashed/landed in water just off Hawaii, which had no real significance, but the story was repeated in the media over and over for 3-4 days and claimed to be reason for stock tanking again…

Are comments not processed after 9 Jun for this story? I submitted comment yesterday suggesting doing an expose on Boeing price manipulation downward over past 2 weeks (likely naked shorting by market maker/big brokerages/dark money pools), but it disappeared today/or is being evaluated?

LK: Takes a day for me to read/ok comments. This is to block spam. Should be up now.

Wonderful article, thanks for putting this together.

As always, thorough coverage backed by undeniable facts. Thank you Lucy

The United States government is so corrupt the people in power do nothing to regulate the SEC on doing their job. The SEC lets hedgefunds get away with controlling stock prices. We have seen this daily. If a multi billion dollar company buys another multi billion dollar company in the past their stock would shoot up! Today between Citadel and the other 3600 hedgefunds in the United States would short and naked a stock so much they can actual hold a stock at the exact price they want or they can bring it all the way down. The SEC does nothing to protect the retail investors, the normal everyday working parent. They let the hedgefunds corruption destroy millions of lives around the country taking their money.

And these are the reasons I’m leaving the country.

WHAT LAWYER WOULD HELP A WOMAN WHO COULD PROVE THE SEC WAS INFACT DOING INSIDER TRADING. PLEASE REPLY

the truth is never hidden. Most don’t look, don’t care to look. Humans are so distracted by Johnny depp, kardashians, their phones, to notice or care

Pingback: Special Solari Report: Game Stop & Naked Short Selling with Lucy Komisar – The Komisar Scoop

Pingback: WTF is the SEC? Is it a Scam? – No Safe Bets

Pingback: “The Lehman Trilogy” compelling 124-year saga of financial giant killed by corrupt system it helped build : The Komisar Scoop

Lucy.

I, William V Marino CPA, won a lawsuit against Merrill Lynch in 1988 that occurred over 10 days over a 2 year period from 1987-88. I also discovered that the SEC was involved in covering up the Crime of the Century.

I have a 2,000 page transcript of my case that was adjudicated before the NASD arbitrators that I am now working on to publish. What occurred in the arbitration hearing will make the Mafia look like Boy Scouts.

Google my name William V Marino CPA SEC and you will be able to retrieve the email I sent to the SEC Chairman Levitt that was in response to his request that CPAs should do more to uncover fraud. I titled my response “You Have Got To Be Kidding”. that was mistyped. I went on the say I uncovered a major fraud and you the SEC covered it up.

The SEC sent an Amicus Curiae to the US Supreme Court in the Shearson McMahon case supporting the NASD arbitration for adjudicating Wall Street customers’ complaints. Ira Sorkin the former head of the Northeast region of the SEC announced after leaving the SEC that Self Regulation NEVER WORKED.

The NASD destroyed their transcript of my lawsuit. Merrill Lynch knowing I had a copy of the transcript was concerned that my copy will reveal the Crime of the Century.

Everything, From A-Z, is corrupt

It is time for a Revolution! A handful of people are screwing over every retailer in the 50 united states. There are too many of us too let them get away with this. WAKE UP AND BE READY TO ACT.

The SEC is corrupt… The good news is that you CAN’T NAKED SHORT CRYPTOS, in fact, its impossible, cryptos cut out all of the crooks and intermediaries… as the largest transfer of wealth happens in our lifetime into cryptos it will collapse the legacy stock markets since as money pulls out it will leave the hedge funds high and dry, not able to cover their positions and trade the paper around to the many clearing firms they each own… the DTCC and CEDE will lose control… it only takes 1% of the population to start a revolution and that has already happened…. crypto gives the power to the people and not the 1%, Central Banks, DTCC/CEDE and their corrupt SEC henchmen..

A must watch video on just how corrupt the SEC is…

https://www.reddit.com/r/Superstonk/comments/v5hsj4/sec_corruption_their_job_is_to_protect_wall/

Bernie Sanders is the only person I’ve heard that’s willing to address this corruption.

Pingback: They Will Take Away The BUY BUTTON Again UNLESS... The Revolution Will Not Be On YouTube. AMC & GME - FIRE-RULES

Well, over the past few years I discovered three corporations, Tyson Foods, New York Times and Pilgrim’s Pride, that are guilt of filing contradictory SEC Reports. They have known of the sins of Tyson Foods since 2002 and 20158 for the other two. Worse yet are those who know and did nothing like Pelosi, Harris, Biden, and Schumer.