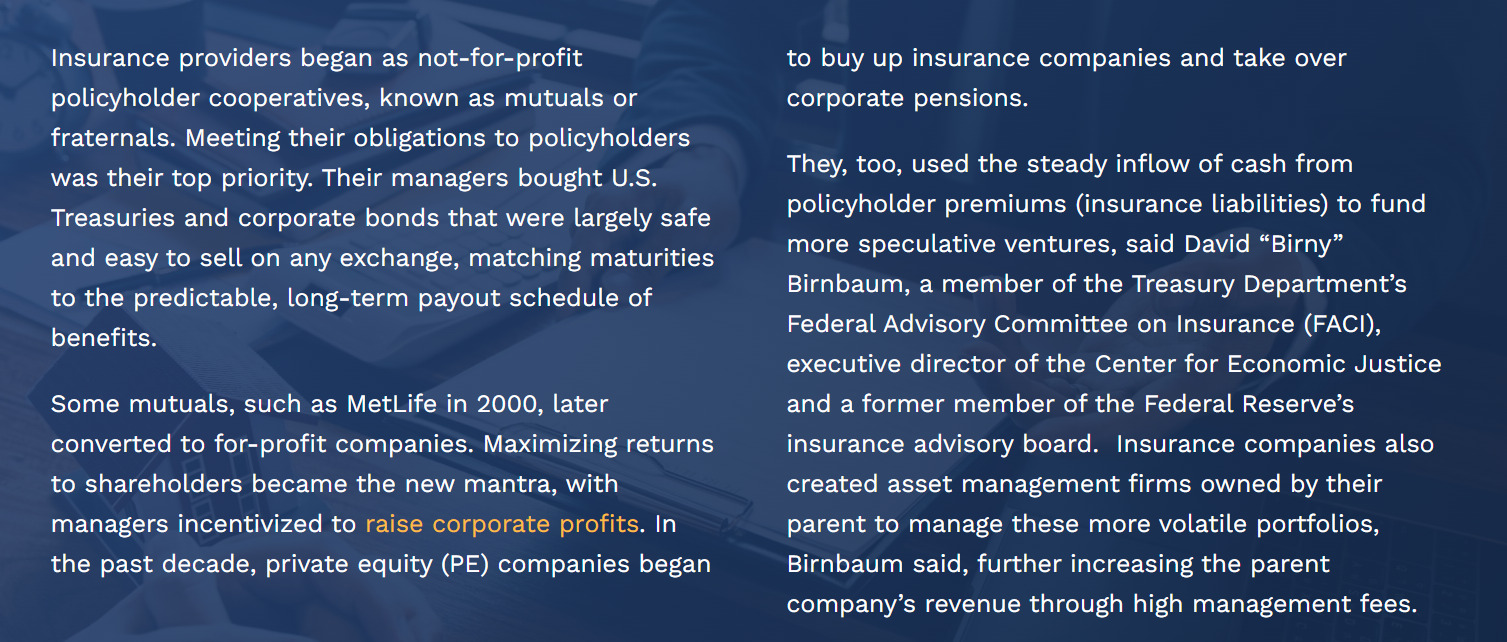

These strategies are part of a broader industry shift as insurance mutuals become publicly-traded companies. Private equity firms, too, have entered the insurance business and assumed greater control over corporate pension funds.

Their actions have prompted Federal Reserve economists and trade unions to issue warnings about investment strategies that, they say, heighten risk for millions of insurance policyholders. These concerns are amplified by the significant role that insurance companies and private equity are playing in credit markets since the 2008 global financial crisis, with little federal oversight.

The companies involved include giants of the insurance industry: Athene Life & Annuity Company, owned by Apollo Global Management Inc., one of the world’s largest asset management and private equity companies; Metropolitan Life Insurance Company (MetLife), the country’s largest life insurance concern; and Accordia, purchased last year by KKR & Co. Inc, also known as Kohlberg Kravis Roberts, the multi-billion-dollar investment and private equity firm. Together, these companies account for roughly one in six life insurance policies and annuities written in the United States.

The three, not alone in the industry, are diverting insurance liabilities into offshore entities, where oversight is scant. They use funds from policyholders to create credit products and buy other types of investments that are far less liquid than traditional investments and carry more risk. These include:

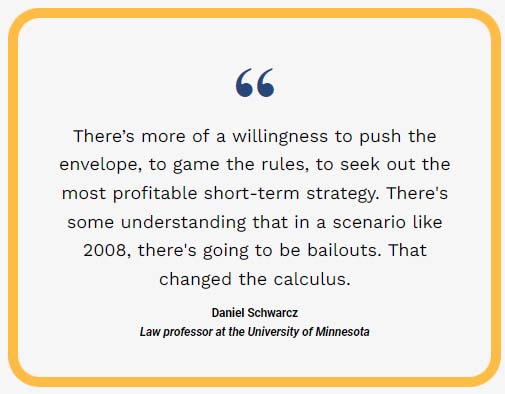

Driven by the growing involvement of private equity, giants of the industry are seeking quick returns, said Daniel Schwarcz, a law professor at the University of Minnesota and an expert on insurance regulation. And in the aftermath of the 2008 financial bailout and rescue of the insurance giant AIG, a number of insurance companies have increasingly abandoned traditional investment strategies that had a long-term horizon in the belief that the government will step in if things go bad, he said.

Daniel Schwarcz

Raising corporate profits: private equity sees life and annuities as an enticing form of permanent capital.

“Life insurance historically invested in bonds. You buy a term life policy, 20 or 30 years, the company buys a bond for 30 years that matches the liability to that asset. And they are liquid, you can sell bonds,” Birnbaum said. But that has changed under new Wall Street owners.

“The business model is based on fees for managing assets. They’ve increased the risk of investments significantly,” he added, pouring more money into collateralized loan obligations and “more exotic types of investments.” These investments are less liquid and more volatile, he said.

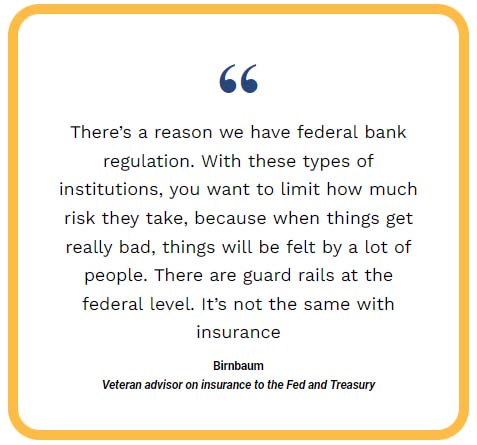

David “Birny” Birnbaum

The trade union Unite Here has warned of a growing risk to the pensions of its members, citing the growing reliance on less liquid asset-backed securities and alternative investments to drive higher returns, the use of investment management agreements with their own affiliates, and the reinsuring of liabilities offshore. Unite Here has flagged the risk of systemic financial collapse.

“We believe that it will ultimately require state, federal and international regulators working together to protect the public from the risks of large life insurer insolvencies and/or contagion to the larger financial system to which they are interconnected,” Unite Here said in a June comment to the National Association of Insurance Commissioners (NAIC), which sets guidance for state regulators overseeing the industry.

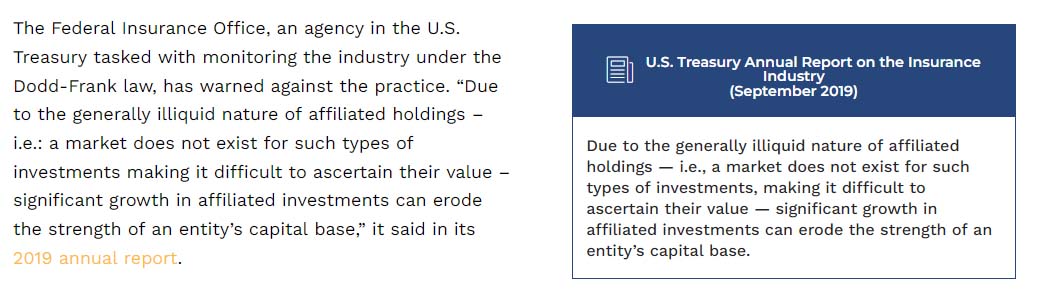

In a September 2021 report, the NAIC Financial Stability Task Force noted that when insurance firms invest in affiliated companies, the firms may increase risk to their own solvency. The same report also pointed out that insurance firms often fail to accurately disclose investments in affiliated companies.

Thomas Gober

This report, the second in a series on how Wall Street is cashing in on the insurance industry, examines three types of risky investments each company uses to boost its profits, drawing from the annual reports filed with the Securities and Exchange Commission and state insurance departments, as well as collateral forms. Thomas Gober, a certified fraud investigator and former Mississippi Insurance Department examiner who has advised the U.S. Department of Justice on insurance fraud, analyzed the relevant documents for 100Reporters.

Bundles of Risk

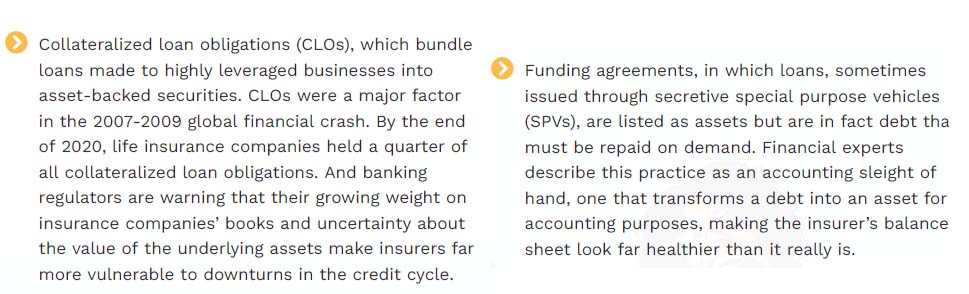

Among structured securities, collateralized loan obligations, or CLOs, are considered the most complex, least liquid and highest risk asset category. The CLOs usually are pools of corporate loans with low credit ratings, or loans taken out by private equity firms to conduct leveraged buyouts. The loans are bundled together to create a high-yield debt instrument structured into tranches, based on the cash flow and on the riskiness of the underlying loans, with higher ratings for tranches claimed to be the most secure. Nobody except the seller knows exactly what’s in them. What is known: None of them are as safe as government bonds.

The rapid growth in the trade of such structured securities recalls developments in the U.S. sub-prime mortgage market in the run-up to the 2007-2009 global financial crisis, the Bank for International Settlements (BIS) said in its 2019 quarterly review. Like CLOs today, sub-prime mortgages in the 2000s were cut into tranches with varying levels of risk, and they were rated by credit agencies.

Athene Dives In

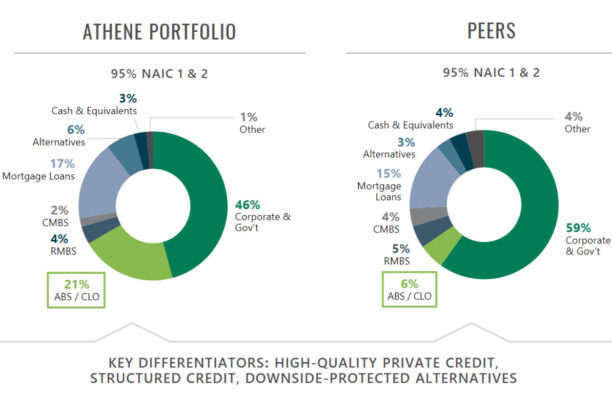

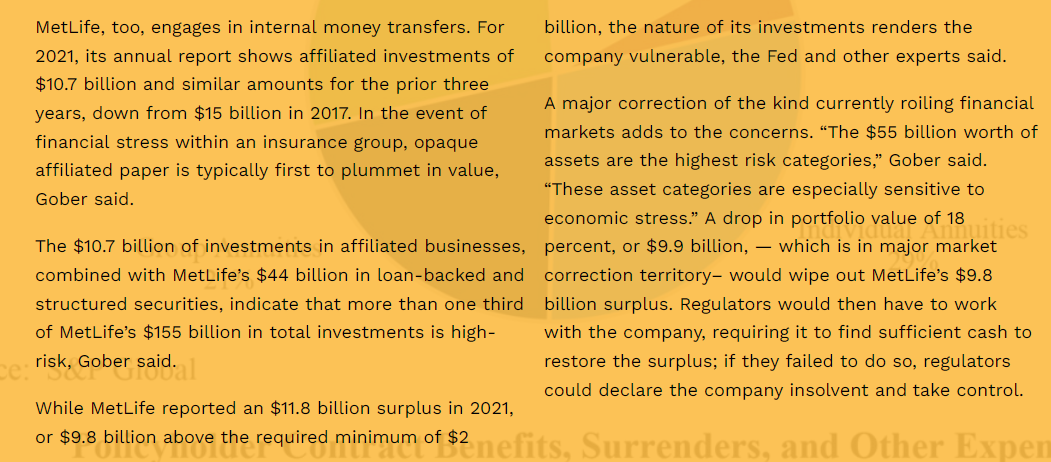

Despite these warnings, a sizable part of Athene’s investment strategy includes buying loan exposure through CLOs. They accounted for 10 percent of Athene’s portfolio in 2022, while other types of asset-backed securities made up 11 percent, according to Athene’s report to investors. Add residential and commercial mortgage-backed securities of 6 percent, that makes 27 percent — or nearly $50 billion, over a quarter of its investments — in riskier assets that are known to face declines in periods of economic stress. Even a slight market downturn could overwhelm Athene’s $1.27 billion surplus, said Gober. (Surplus is the amount of assets over liabilities the company must hold below which regulators can rule it insolvent.)

Athene invests more in high-risk collateralized loans and asset-backed securities

Athene’s exposure is 21 percent for asset-backed securities (ABS) and CLOs, over three times higher than its peers, which had 6 percent.

The NAIC Financial Stability Task Force in its September 2021 report expressed concern about the concentration of asset-backed securities in the holdings of private-equity owned insurance companies. “[P]rivate equity]-owned companies focus far more on investing in asset-backed securities (ABS) than the industry as a whole: 25 percent vs. 10 percent of total bonds in 2020,” the task force said.

The Fed economists in their 2021 report cited Athene, among others, in noting that “these life insurance companies hold some of the riskiest portions of the CLOs issued by their own affiliate asset managers.” It added that “a widespread default or downgrade of risky corporate debt could force life insurers to assume balance sheet losses of their CLO-issuing affiliates, wiping out their equity.”

MetLife Exposure

MetLife has a similar high exposure to risky investments. Its 2021 annual financial report shows $16 billion listed under “Other loan-backed and structured securities.” Gober, the insurance investigator, said these include CLOs and student and credit-card loans bundled into asset-backed securities known for their higher default rates. In addition, MetLife reported its residential and commercial mortgage-backed securities were more than $27 billion, bringing riskier investments to $43 billion. MetLife’s surplus, at $11.8 billion, is just under 3 percent of total assets, or half of the national average for insurance companies.

These investments have caught the attention of Fed economists, who said in their 2021 paper: “U.S. insurers returned to RMBS (residential mortgage-backed securities) issuance in 2017, though issuance levels remain low relative to CLOs. The two main players in this relatively niche market are AIG and MetLife.”

John Patrick Hunt

John Patrick Hunt, professor at the University of California, Davis and a former regulatory lawyer and litigator who specializes in the financial regulation of insurance companies, told 100Reporters, “MetLife seems to be taking on the riskiest pieces of complex products called CLOs, as well as using Bermuda captive reinsurers, to reduce the equity U.S. regulators would otherwise require the companies to hold to cover losses.” He said such moves increase the risk that investment losses could make the insurance conglomerate insolvent, and ultimately unable to honor its commitments.

Books in Bermuda are largely secret, so the public doesn’t know the details of what investments those companies hold. Scholars and regulators have identified ways in which the financial distress of a large insurer like MetLife could ripple through the entire financial system. “Large insurance conglomerates historically have had obligations to other systematically important financial firms such as major banks,” Hunt said. “If the insurer fails and can’t honor such contracts, that could contribute to the failure of the other party to the contract in a falling-dominoes effect similar to what we saw in the global financial crisis,” Hunt said.

MetLife’s head of communications Dave Franecki emailed, “We appreciate you reaching out and walking through some of the themes.” But he declined to comment further: “MetLife is not going to provide an interview or comment for your story or the related series of stories being published by 100Reporters,” Franecki said.

ACCORDIA, started by Goldman Sachs, sold to KKR

Accordia is a small company compared to Athene and MetLife. Last year, the private equity firm KKR purchased a majority stake in Accordia’s parent company, Global Atlantic, from Goldman Sachs. Global Atlantic is based in the Cayman Islands, where books are largely closed to the public and profits shielded from US taxes.

In its 2021 Schedule D bonds filing, which is part of its annual financial report, Accordia lists $2.5 billion under “Other Loan-Backed and Structured Securities”, which includes CLOs.

Funding Agreements, or Handy Tricks for Turning a Liability into an Asset

Funding agreements are short-term investor loans, which can appear on the insurance company’s balance sheet as an asset when in fact they are debt obligations. They generally are issued through a shell company known as a Special Purpose Vehicle (SPV) or Special Purpose Entity (SPE), which issues a note on behalf of the insurance firm. Investors buy the note from the SPV or SPE, which passes the money on to the insurance firm.

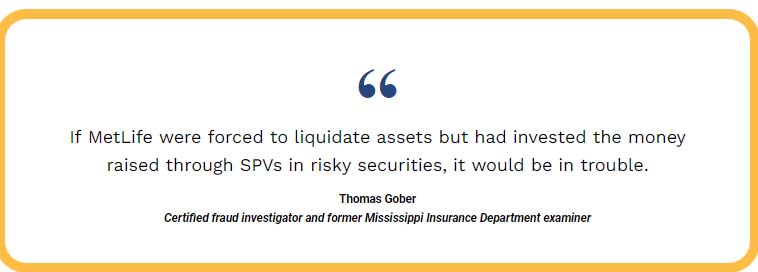

Spared from public disclosure requirements, SPVs played a major role in the 2008 financial crisis. “The SPV is off-balance sheet and under-regulated,” Gober said. “The SPV is a shell that impedes regulatory oversight and improves the insurer’s financial appearance.”

The SPV is off-balance sheet and under-regulated. The SPV is a shell that impedes regulatory oversight and improves the insurer’s financial appearance.Thomas Gober Certified fraud investigator and former Mississippi Insurance Department examiner

Why does the insurance company run this deal through an SPV? Doing so allows insurance companies to report such debts as “insurance products,” lowering the reserves they must hold against their eventual payment. On the balance sheet of the insurance company the influx of funds appears as an asset when the money is invested in securities. In reality, however, it is also a liability, because the money has to be paid back.

By lowering the reserve requirements, the insurance company frees up more cash to invest, said a senior government policy advisor on insurance, who spoke on background because he lacked authorization to speak to a journalist. But these loans are short-term and can be readilyrecalled, making the insurance companies less resilient to volatility in the marketplace.

Financial experts say a similar set of financial conditions prevailed during the banking crisis of 2008. At that time, plunging loan markets caused lenders to request their money back on short notice, forcing companies to liquidate their assets, which triggered a cascade of selling. SPVs were especially hard hit. Aggravating the damage, investors and regulators had little visibility into their risk, especially for SPVs held in offshore subsidiaries where financial disclosure is scant.

Funding agreements heighten risk for policyholders in another way. In the event of bankruptcy, insurance policyholders usually are the first in line to get paid. But under the terms of these funding agreements, the loan investors are deemed of equal standing with policyholders.

If the insurance company becomes insolvent, policyholders must compete with investors for the leftovers. And because of secret side agreements that give private equity companies wide discretion for favoring friends, relatives, and some select investors over others, policyholders and pensioners will have less standing as they compete for the remaining crumbs.

The Fed economists in their 2021 paper raised a red flag about these types of loans in particular. “These funding activities render the insurer vulnerable to runs,” the Fed economists wrote. “During the financial crisis, runs on insurers forced them to scramble for liquidity from other sources, including FHLBs [Federal Home Loan Bank]. In some cases, insurers required substantial government assistance to prevent spillovers to households and to the rest of the financial system.”

Despite the 2008 crisis which led to the taxpayer bailout of AIG, insurance companies have managed to remain outside federal regulation of the industry, leaving oversight to a patchwork of states, some of which have become havens known for lax oversight.

The latest filing by Athene says that none of its funding agreements allow discretionary, or on demand, withdrawals, which could cause a run during a steep market decline. MetLife says a small number allow them. However, the senior government insurance policy advisor asked, “What does discretionary mean? Is the term a long term? It’s feasible that fixed means a month. Or let’s say they are fixed for a year but they are staggered. At any point some are coming due.” The companies’ filings report their funding agreements but don’t answer those questions on their maturity dates.

Gober analyzed how funding agreements are reported as income, rather than debt, by Athene and MetLife.

In the section for reporting liabilities on its 2021 annual statement, Athene listed nothing on line 22 under “Borrowed Money”. It is blank, showing zero debt.

But in another part of the annual statement for 2020, called Schedule T for reporting on premiums and annuity, there’s a hidden debt of $1.8 billion called “deposit-type contracts,” which are funding agreements – or loans issued through SPVs.

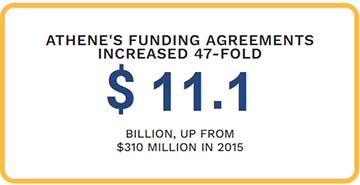

This is not income but a form of debt, though Athene doesn’t report it as such. By 2021, funding agreements, shown in column 7, had increased 47-fold to $11.1 billion, up from $310 million in 2015, dwarfing Athene’s $1.2 billion surplus. Athene announced it was the largest issuer of funding agreements across six different currencies.

According to Athene’s filings, nearly all of the $11.1 billion raised through funding agreements and listed as insurance products is sent to reinsurance, much of it to lightly regulated affiliates or offshore, where secrecy reigns; it is unknown how much is invested in illiquid assets, of the kind the Fed warned of in its report. A sudden demand for the cash could be dangerous, Gober cautioned. In the face of massive losses, Athene’s nearly one million policyholders seeking claims would be standing in a very long line for payouts, absent significant government intervention.

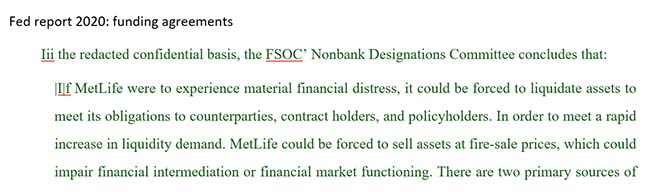

Government economists long have expressed concern about MetLife’s heavy reliance on funding agreements, going back to the creation of the Financial Stability Oversight Council (FSOC) in the U.S. Treasury, in the aftermath of the 2008 global financial crisis. The FSOC was charged with detecting conditions that could threaten the country’s financial system and was given authority to audit and assess not only banks but other large financial companies, including insurance companies. If FSOC considered a firm vital to the safe functioning of global markets, it was assigned a red flag and labeled “systemically important financial institutions” (SIFIs).

Along with AIG and Prudential, MetLife was a focus of the Financial Stability Council’s’s investigation and was designated a SIFI, on the grounds that the collapse of any one of these companies could devastate the financial system. The financial stability council noted in a 2014 report that MetLife’s funding agreements made it vulnerable, since it issued 75 percent of the $50 billion market for funding agreements (FA) and FA-backed securities issued by U.S. life insurers in the first six months of 2013. In a financial downturn, creditors could immediately call that money back, forcing MetLife to liquidate assets at fire-sale prices, which would affect the wider markets, the Financial Stability Oversight Council said in its 2014 report.

Despite this warning, MetLife reported $30 billion in funding agreements in 2018, and its latest financial filing shows the insurer had increased that to $72 billion in 2021, listing them as “deposit-type contracts.” Its website shows that it is actively promoting these instruments as a retirement solution for clients.

Instead of calling this borrowed money, MetLife lists funding agreements on its financial statement alongside premiums. It describes these contracts as “holding the Deposit for the benefit of the Beneficial Owner.” Gober pointed out this is a convoluted way of describing a loan, since the beneficial owner is the creditor, not MetLife. He noted that by 2021, funding agreements dwarfed by three-fold MetLife’s worldwide business of $24.3 billion in premiums, shown on column 6 of its Schedule T. According to its filings, Gober noted, MetLife is borrowing three times as much money as it takes in as premiums.

MetLife’s Fight Against Federal Oversight

FSOC case against MetLife

MetLife fought back against the financial stability council’s too-big-to-fail designation. It hired lawyer Eugene Scalia, then a partner at the law firm Gibson, Dunn and Crutcher and son of Supreme Court Justice Antonin Scalia. (The younger Scalia would go on to become Labor Secretary under Donald Trump.)

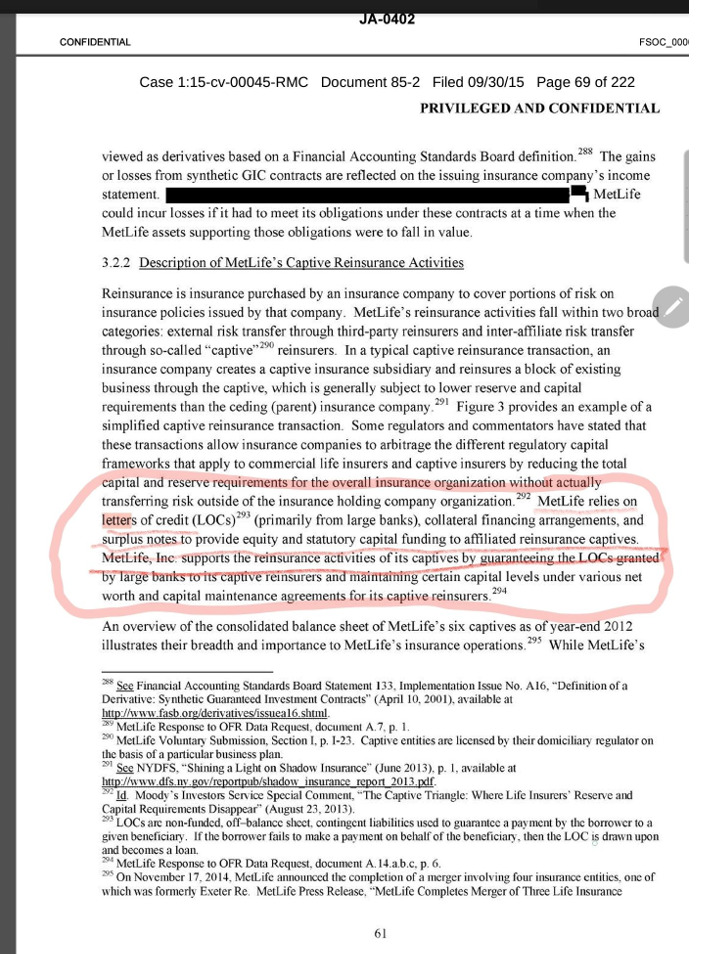

In a suit against the Treasury Department, MetLife argued that the FSOC used a flawed argument to determine that its collapse could devastate the financial system. It insisted that captives funded in part by letters of credit did transfer risk. And it argued that as it already operated under a strict state regulatory system, that non-bank SIFI regulation put it at a disadvantage against its competitors. MetLife maintained that the financial stability council should address the risk posed by specific systemic activities rather than by the size of companies. The case was brought during the Obama administration.

In 2016, U.S. District Judge Rosemary Collyer, a President George W. Bush appointee, overturned the designation, rejecting that MetLife was systemically important to the U.S. financial system and “too big to fail,” and determining the council’s decision was “arbitrary and capricious.” The judge accepted MetLife’s argument, and ruled the Financial Stability Oversight Council: “never established a basis for a finding that MetLife’s material financial distress would ‘materially impair’ MetLife counterparties….FSOC never projected what the losses would be, which financial institutions would have to actively manage their balance sheets, or how the market would destabilize as a result….FSOC was content to evaluate interconnectedness and to refrain from calculating actual loss, i.e., to stop short of projecting what could actually happen if MetLife were to suffer material financial distress.”

Trump ends federal oversight of insurance industry — Biden administration doesn’t challenge this

FSOC, by then chaired by President Donald Trump’s Treasury Secretary Steve Mnuchin, a former Goldman Sachs banker, didn’t appeal. Mnuchin also removed the SIFI designations from the insurance giants AIG – which had contributed to the 2008 financial crisis — and Prudential. In December 2019, Mnuchin issued new guidelines changing the SIFI criteria: instead of identifying institutions that pose systemic risk to the financial system, the government would identify certain types of investment activities that merit special monitoring. Today there are no financial institutions outside the banking sector designated as SIFIs, despite a major expansion of their credit intermediary role in the financial system. After the decision, FSOC regulatory oversight of the insurance industry was constrained and left to the states.

A senior Biden administration official, who worked on the FSOC designation process and requested anonymity because the official was not authorized to speak publicly, told 100Reporters that insurance oversight has not changed under the current administration. “We have not gone back and been aggressive,” the official said, adding there is a lack of “courage and backbone” to take on the insurance industry. This has caused mounting frustration among some Democrats on Capitol Hill.

MetLife has continued the practices that raised red flags over a decade ago.

The smaller Accordia does not have the financial size to borrow billions of dollars through funding agreements.

Shuffling Funds to Shell

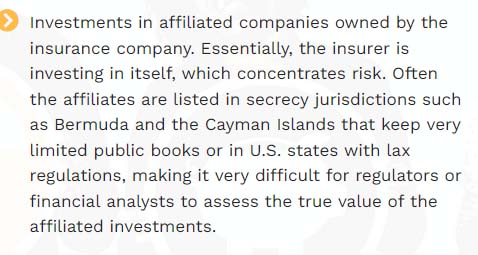

Companies normally buy stocks and bonds in the open market, where prices are transparent and based on perceived risk. But there is a second strategy some insurance companies are using. It works like this: the insurance company sends $1 billion in cash to a related company which doesn’t have audits, isn’t publicly traded, and is, in fact, a shell. In return, the insurance company receives an internal IOU, which it calls a bond but which is not a marketable security. No one outside can see the paper trail. Essentially, the insurance company is buying a piece of itself and counting that as an investment.

Gober said this lack of transparency is especially concerning for insurance companies that have subsidiaries in US states with lax regulations and offshore where they dump billions of dollars of investments that cannot be overseen because their books are largely shielded from public scrutiny. Outsiders cannot assess the level of risk, he said.

Two years later, the NAIC Financial Stability Task Force warned in its September 2021 report that state regulators may be failing to adequately assess the risk from this practice. “Affiliated transactions are considered by regulators, but it is not clear if all appropriate PE (private equity) transactions are captured,” it said.

Hidden Gamble

Apollo Capital Management has used its affiliated companies in questionable ways for at least a decade. Athene’s annual statement for 2014, for example, shows that in 2013 it made an investment in an Apollo affiliate to disguise a bailout of Caesar’s and Harrah’s casinos, which subsequently went bankrupt.

Under a Nevada law passed to keep out organized crime, changes in casino ownership must be approved. In July 2013 the Nevada State Gaming Control Board heard a proposal to transfer an interest in Caesar’s Entertainment to Apollo. A lawyer for Caesar’s said, “This is essentially an investment by Athene indirectly in Caesar’s.” Five months later, Athene bought AAA Investments (Co-Invest VI). Nobody reading Athene’s financial statement would know that AAA Investments was a vehicle for funneling money to two risky Nevada casinos.

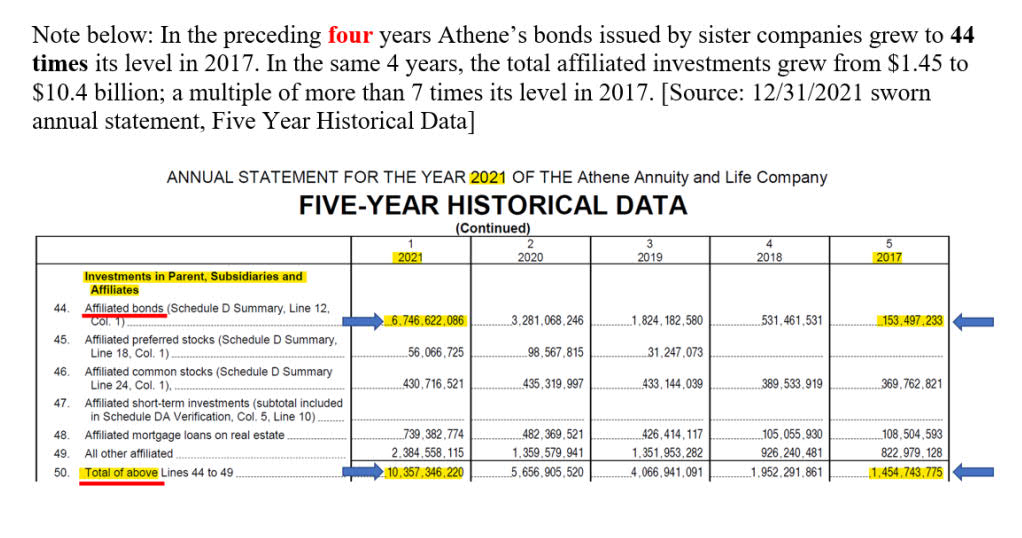

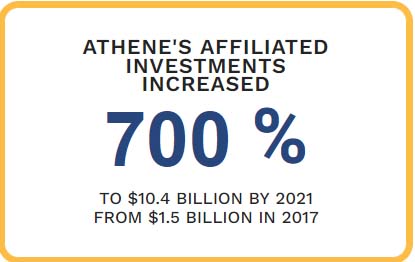

Since then, the practice of affiliated investments has ballooned. In a four-year timespan, Athene’s purchase of affiliated stocks and bonds increased 700 percent to $10.4 billion by 2021 from $1.5 billion in 2017, according to its annual statements. Athene declined requests for comment.

ATHENE’S AFFILIATED INVESTMENTS

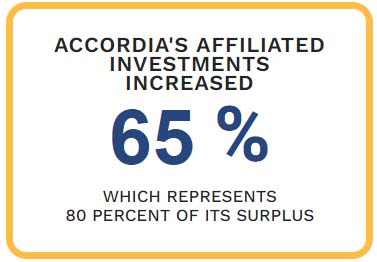

Accordia’s affiliated investments for 2021 are $758 million, or 6 percent of assets, substantially higher than in past years. While its total assets ($12.739 billion) and liabilities ($12.709 billion) have grown from 2020 to 2021, its surplus has shrunk relative to liabilities, which it has to cover.

Companies in an agreement reached with the NAIC are allowed to determine the level of risk-based capital they hold as a buffer to ensure they can meet their liabilities. The figure Accordia set in its 2021 financial statement was $141.8 million. It is the bare minimum that must be covered by the surplus.

Accordia’s affiliated investments for 2021, a 65 percent increase over the year before, represent 80 percent of surplus. Were a substantial number of affiliated investments to decline sharply in value, Accordia could be ruled insolvent, though its owner has the option of providing the missing cash. Combined with its structured loan portfolio, Accordia’s high-risk investments total $3.8 billion, leaving Accordia’s buffer vulnerable to an economic downturn, Gober said. Accordia declined requests to comment.

Rich Returns

Executives and shareholders of for-profit life insurance companies and their private equity owners can benefit generously from investment strategies that pour cash into higher risk assets.

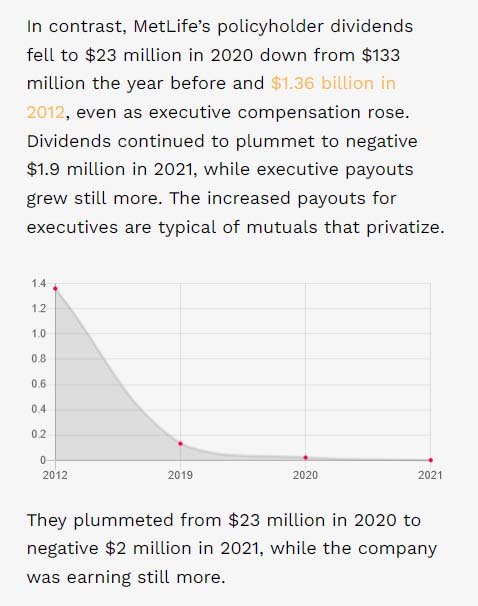

As a mutual, policyholders were owners and they received dividends from MetLife, for example. When executives proposed it demutualize, or transform itself into a for-profit company, they won policyholder approval in part by promising that they would continue to receive dividends. They did, but their value went down to virtually nothing.

MetLife’s stock price has tripled to $71.47 over the last decade outpacing the overall gains in the broad stock market, and annual dividends to stockholders have risen from 60 cents a share in 2013 to $1.96 today. These gains have enriched its Chief Executive Officer Michael Khalaf: he enjoyed a 25 percent increase in his base salary to $1.35 million between 2019 and 2021, plus a 28 percent increase in stock and stock options awarded, bringing his total compensation last year to $16.62 million. Three of his top executives have received similarly rich rewards.

Athene found an extra way to reward its Chief Executive Officer James Belardi. In addition to his compensation package from Athene, Belardi owned a 5 percent stake in the investment management company set up by Apollo to handle Athene’s assets, which meant he benefited directly from the fees paid by his own company. Moreover, the Financial Times reported in 2018 that an internal investigation showed Athene was paying its investment management firm twice as much as an independent manager would charge for similar services – 0.3 percent of assets under management compared with 0.15-0.25 percent for an unaffiliated manager. Athene, which declined to comment for this article, has elsewhere defended the high fees, telling the Financial Times, “Apollo has sourced investment opportunities for Athene that other managers simply can’t provide, including some of our most successful investments to date.

What’s at stake

The investment practices described here represent dangers to policyholders on several levels should an insurance company grow insolvent, said Birnbaum, the veteran advisor on insurance to the Fed and Treasury. Even though state guarantee funds exist to cover policyholder losses, most states have caps of $250,000-$350,000. People who have paid higher premiums for more insurance or anticipate retirement annuities may lose much of their investment.

Additionally, guarantee funds are based on the premise that the failure of one company is absorbed by others. States recoup the cost through a surcharges, which then get passed onto policyholders through a surcharge. But state regulators may be under-estimating the risk.

“Abusive and deceptive sales — the domain of market regulation, not solvency regulation — can lead to solvency issues,” Birnbaum said. “That’s exactly what happened during the financial crisis with bond and mortgage insurers.

“The competition for these insurers to get the business of bond issuers and mortgage originators led to abandonment of risk management by the insurers that solvency regulators missed,” Birnbaum said.

“There’s a great danger because the financial regulators look at solvency solely from the perspective of a company going insolvent – Do they have adequate reserves? Do we have adequate oversight? That limited vision was exposed during the (2008) financial crisis,” he said.

There is also a risk that other parties to a transaction will not be able to fulfill their obligations. “It’s not just one company. If they’re all doing it, it’s all connected. If there are numerous significant failures, the guarantee fund system won’t be able to handle that,” Birnbaum said. Nor would the financial system.

Schwarcz, who was the lead author of the legal brief filed by insurance regulation scholars in support of the government’s move to oversee MetLife, said risk is compounded because insurance companies today are deeply interwoven with global credit markets. When a counterparty demands its money back on short notice, can the insurer liquidate assets quickly enough to repay?

“Unfortunately, it’s rather opaque,” Schwarcz said. In the past, financial companies that engaged in high-risk strategies have dipped into taxpayers’ pockets. Insurance conglomerate AIG survived the 2008 crash only with an $85 billion bailout by Federal Reserve Bank of New York..

Birnbaum fears a repeat. “As the products become more complex and riskier, there’s greater likelihood the [state] regulators don’t fully understand the risk and can’t stay on top of it. We’re talking about trillions of dollars of assets held by life insurers.”

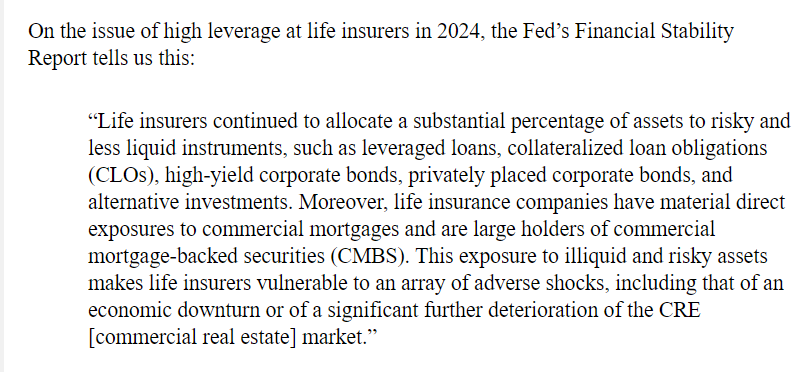

Added Dec 3, 2024, new report by Federal Reserve (pages 31-32 of print):