By Lucy Komisar

The Realist Review, Feb 15, 2026

Among the nine people Donald Trump named to his Board of Peace to run Gaza – which holds its first meeting in Washington DC February 19 – is billionaire private equity operator Marc Rowan. The board’s stated tasks include establishing financial controls and managing the reconstruction of a Gaza. You might think a savvy financier would bring solid credentials to such a job.

You would be wrong.

Let’s start with the obvious: this “Board” is little more than a colonial operation—a modern day version of the British East India Company.

And Marc Rowan is a perfect avatar for such an operation.

Rowan runs Apollo Global Management, one of the world’s largest private equity firms, not with prudent stewardship but via a financial scheme that bears the hallmarks of two of history’s most infamous frauds: the accounting chicanery of Enron and the Ponzi dynamics of Bernie Madoff.

And then there is the Epstein connection.

Rowan’s selection signals that Gaza’s future may be handed to a man whose business model is built on opacity, regulatory arbitrage, and extracting value from systems he is tasked with safeguarding.

At the heart of the scheme is Apollo’s insurance subsidiary, Athene. Here’s how it works, and why it matters far beyond Wall Street.

The Executive Life Insurance scam

Apollo was linked to Wall Street corruption from the very start. In the 1980s, Drexel Burnham Lambert—where Marc Rowan was a vice president in the mergers and acquisitions department—stuffed the Executive Life Insurance Company (ELIC) with junk bonds, causing its collapse. In a rigged auction, French interests illegally acquired ELIC. The California Department of Insurance, as the court-appointed liquidator, sued and won a landmark $771 million judgment paid by Crédit Lyonnais and its affiliates. However, Apollo, founded a few years earlier and co-chaired by Rowan, had already bought the stolen bond portfolio from the French at a discount, making billions.

Apollo paid zero restitution.

Rowan had to know the assets were tainted. He was Apollo’s distressed debt expert and personally oversaw the ELIC acquisition. In 1993, the red flags were unmistakable to any sophisticated investor. First, the seller was Altus Finance, a subsidiary of Crédit Lyonnais—which was a French government-owned bank. U.S. law prohibits foreign governments from owning U.S. insurers, and the fact that Altus was reselling the portfolio immediately suggested the original buyer could not legally keep it.

Second, the price was too good: Apollo paid approximately $1.7–2.0 billion for a portfolio with an estimated fair market value of $2.5–3.0 billion. Any competent distressed debt team would ask: “Why is the French government selling these bonds at a fire-sale price only 18 months after buying them in a politically charged auction?” Third, the ownership structure was opaque, involving a web of French shell companies, nominee directors, and secret financing—hallmarks of a concealment scheme. Apollo’s lawyers would have reviewed title documents revealing these complexities. A reasonable investor would have investigated further. There is no evidence Apollo did so.

Apollo did not just profit from the ELIC portfolio—the deal was foundational to the firm’s success. Between 1993 and 1998, Apollo restructured and sold down the bonds, generating billions in profits. These gains helped establish Apollo as one of the world’s largest distressed asset managers. The founders became billionaires. The ELIC portfolio made it all possible. And unlike Crédit Lyonnais, which paid $775 million in fines, Apollo paid nothing.

The corrupt Athene life insurance operation

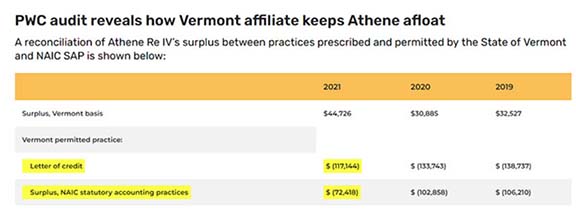

Today, Apollo uses a network of secretive shell companies, called “captives,” in places like Bermuda and compliant U.S. states such as Vermont. Into these black boxes, Athene dumps billions of dollars in liabilities—the promises made to policyholders and retirees. In return, it takes an accounting “credit,” magically reducing the capital it is required to hold.

But this isn’t real risk transfer. It’s moving money from one pocket to another. Worse, to make these shells appear solvent, they are stuffed with “Letters of Credit”—essentially, a bank’s promise to lend money if needed.

Under standard insurance rules, this is a liability, not an asset. But friendly state regulators allow Apollo to count them as real money.

The smoking gun is in the audits.

PricewaterhouseCoopers, Athene’s own auditor, has repeatedly noted that without this fake paper, key Apollo affiliates would be “insolvent” and below legal capital requirements. The entire edifice is propped up by accounting fiction.

This leads to the Madoff-like element: the operation’s stability depends on a constant influx of new cash. Apollo “skims” real policyholder assets, replacing them with these dubious IOUs, and funnels the money into its own risky investment strategies. The reported surplus—the thin buffer protecting millions of policyholders—has remained stubbornly static at around $1.3 billion even as tens of billions in new premiums flow in. It is a structure vulnerable to the slightest tremor.

Rowan is the architect of this strategy, explicitly designing Athene to be a “permanent capital vehicle” funding Apollo’s deals. The inherent conflicts are glaring: Athene’s CEO owned a stake in the Apollo affiliate managing its money, incentivizing him to send more policyholder cash Apollo’s way.

The victims are ordinary people. Corporations like Lockheed Martin and Alcoa have transferred their employees’ pensions into Athene, stripping retirees of federal protections. If this house of cards collapses, these pensioners will stand in line with other creditors, likely losing benefits beyond meager state guarantee caps. And because Athene represents about 40 percent of Apollo’s value, its failure could trigger a systemic crisis, potentially requiring another AIG-style taxpayer bailout.

This is the record of the man now slated to help oversee Gaza’s reconstruction.

The Ghost of Jeffrey Epstein and the Playbook for Gaza

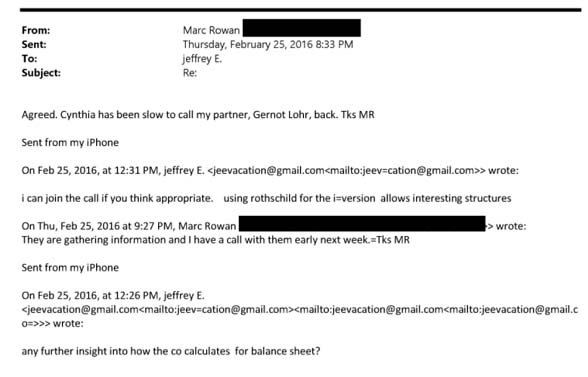

To understand how Rowan would operate in Gaza, one need only look at his past relationship with Jeffrey Epstein. The Epstein files show Rowan sought Epstein’s help on the most aggressive, complex, and high-stakes financial engineering strategies available. See Rowan in the Epstein files here.

Specifically, the emails reveal Rowan and Epstein intensely focused on two key topics:

Corporate Inversions and Tax Receivable Agreements (TRAs). They discussed how to use Rothschild to create “interesting structures” for shifting a company’s legal domicile to a lower-tax jurisdiction, a paper move that maximizes profit while separating economic substance from legal obligation.

Dozens of emails also show them dissecting intricate worksheets for TRAs, complex financial instruments which are designed to monetize future tax benefits into immediate cash, often at the expense of long-term public revenue.

These are not generic business tips. This is the operational playbook for arbitrage and extraction, essentially to cheat a government, in this case by tax evasion — skills Rowan perfected and applied against the U.S. with Athene. Gaza, a territory with no sovereign government, a decimated civil society, and tens of billions in anticipated aid, would present the ultimate opportunity to deploy this playbook.

The reconstruction of Gaza would not be a humanitarian mission under Rowan’s guidance; it would be another deal. His model suggests that Gaza will be rebuilt not for Palestinian life, but as a “permanent capital vehicle” for global investors:

- Financial Controls Designed for Opacity: The board’s mandate to “establish financial controls” mirroring the Athene structure could mean creating a labyrinth of shell companies and SPVs (Special Purpose Vehicles) in places like the Cayman Islands or Delaware. Aid money and future revenue streams (from tolls, utilities, ports) would disappear into this black box, shielded from public oversight.

- Transforming Aid into Debt: Just as TRAs turn future tax obligations into present-day cash, reconstruction would be financed not through grants, but through loans and public-private partnerships. Critical infrastructure would be built by consortia led by firms like Apollo, locking Gaza into decades of debt servicing and guaranteeing investor yields. The liability of rebuilding would be transformed into a financial asset—for outsiders.

- Priority on Investor Returns, Not Palestinian Needs: The capital “freed” by these opaque structures would be deployed, as at Athene, into high-fee, high-risk projects. Reconstruction would prioritize lucrative contracts for connected firms and revenue-generating infrastructure (like desalination plants or telecommunications) that can be privatized, not necessarily homes, schools, or hospitals for displaced families.

The task, if it were honorable, would demand unimpeachable integrity, a commitment to transparency, and a fiduciary duty to the public good. Mr. Rowan, however, demonstrates a mastery of exploiting weak governance, hiding transactions in secret jurisdictions, and prioritizing fee extraction and financial engineering over fundamental solvency.

The board’s mandate requires establishing financial controls. Rowan’s business model is based on subverting them. His reported appointment isn’t just unwise; it telegraphs the Board’s true intentions. Someone who builds wealth by undermining financial governance should not have a role in it in Gaza, if—that is—the board were anything other than a grifting opportunity.

Any credible peace and reconstruction effort demands transparency, integrity, and an unwavering commitment to the public good—values Marc Rowan’s career has consistently flouted. Entrusting him with Gaza’s future sends an obvious message: that this mission of immense moral weight and complexity is just another deal—a territory to be stripped for parts rather than a society to be rebuilt with care and accountability.

Articles about Rowan/Apollo abusive practices

Investigation shows for-profit life insurance industry operates a scam

and

Risky Business: How Insurance Companies are Chasing Profits over Policyholder Security